Student Loans Part 3: The Big Dilemma -- Invest or Pay Them Off? (Ep. 126)

Are you a law firm owner staring down a six-figure student loan balance and wondering: Should I throw every extra dollar at my loans, or should I invest that money for long-term wealth? This is a dilemma faced by many successful attorneys. On this episode, we’ll break down the key considerations you need to think of so you can confidently decide what’s best for your financial future and your firm.

Understanding Opportunity Cost: The Key to Smarter Money Decisions

Let’s start with a cornerstone of smart business decisions: opportunity cost. Simply put, opportunity cost is what you give up when you choose one financial option over another. That means every time you pay down debt rather than invest in your retirement, your firm, or even your well-being, you’re making a trade-off. The real question isn’t just “Should I pay off my loans?”, it’s “What could I be doing with this money instead?”

Here are a few alternatives to aggressive debt payoff:

Investing in retirement accounts that benefit from compounding growth

Building a marketing strategy to grow your client base

Hiring staff to free up your time for higher-level work

Purchasing real estate for passive income

Even taking a vacation to recharge and avoid burnout

Paying down debt feels good because it’s safe, simple, and provides immediate results. However, that’s not always the highest return on your money especially when your loans carry a lower interest rate compared to your other opportunities.

The Math: Running the Numbers on Debt vs. Investment

Let’s talk numbers. The logical side of the decision compares interest rates on your debt to the potential return on investments.

Example from the podcast:

Suppose you have $150,000 in student loans at a 6% interest rate. If you add just $500 a month to your payments (for a total of $1,500/month), the debts could be paid off in 12 years.

But what if you invest that $500/month instead?

Assume a modest 9% annual return in a low-cost S&P 500 index fund. Over 12 years, you could accumulate about $130,000—enough to pay off the remaining loan balance and still have roughly $33,000 left over.

In this scenario, investing gives you a better financial outcome, assuming market returns hold and you are comfortable with their inherent risks.

Beyond the Numbers: Understanding Your Risk and Psychology

While the math lays out the financial logic, your decision must also align with your comfort level, priorities, and mindset.

Ask yourself:

Does having debt stress you out, even if it’s not the most profitable choice to pay it off?

Would eliminating your loans help you sleep better, regardless of potential higher returns elsewhere?

Or, are you energized by watching your investments grow and your financial freedom increase over time?

As discussed in the podcast, our brains are wired to prefer quick wins (the so-called “hyperbolic discounting”), which explains why debt payoff feels so satisfying, even if the math suggests otherwise.

Tips to Outsmart Your Financial Biases

If you want to leverage your dollars to their fullest potential, yet not fall prey to short-term thinking, try these strategies:

Automate Investments: Set up regular, automatic contributions to investments so you don’t have to overthink it.

Celebrate Milestones: Reward yourself for investing, not just for making extra loan payments.

Visualize Your Future Self: Picture what your life and business will look like in 10, 20, or 30 years based on the choices you make now.

Focus on Identity: Remind yourself, “I’m a business owner who makes strategic decisions with my money.”

Not Deciding Is a Big Decision

Ignoring the question altogether is the costliest mistake. Delaying action whether it’s on refinancing your loans when rates are favorable, or starting to invest—means missed opportunities and potentially higher debt costs.

Enter to win:

The Lawyer Millionaire Listener Challenge

Resources:

{kind=link}

Connect with Darren Wurz:

Transcript:

Darren Wurz [00:00:00]:

Would you rather save $30,000 in loan interest or grow $300,000 in investments? Welcome to the Lawyer Millionaire helping law firm owners grow their businesses and their wealth. I'm your host, Darren Wurz. You know, student loan decisions aren't just about numbers. They're about psychology. And the truth is your brain is wired to sabotage the smart choice. That's right, my friends. Today we're unpacking how to actually make the best student loan decision using real math, behavioral science, and high impact examples. Because when you understand the true cost of your choices, you can finally build a strategy that serves you.

Darren Wurz [00:00:41]:

Hey there, lawyer millionaires. Before we dive in, I want to quickly tell you about our Lawyer Millionaire listener challenge. All you need to do is leave a review and share your favorite episode with a friend or on social media. Then head on over to lawyermillionaire.com/challenge to submit your proof. And you'll be entered to win a $100 gift card, a signed copy of my book, and even a private strategy session with yours truly. The link is in the show notes. Let's go. Get your entry in today.

Darren Wurz [00:01:12]:

All right, now, on with the show. So let's say you're staring at a six figure student loan balance. You're doing the avalanche method. Maybe you're thinking about refinancing, but somewhere deep inside you're wondering, am I making the right choice or just the one that feels right in the moment? This episode isn't about which repayment strategy saves the most money. It's about how to think about your decision. And we're going to get into, you know, more than just a yes or a no. We're going to talk about the frameworks and the psychology that help you make the best choice. Okay.

Darren Wurz [00:01:43]:

Before we dive in, we need to understand a key concept, and it's this opportunity cost. If you haven't heard that word before, ooh, you're in for a treat. So opportunity cost is what you give up by choosing one option over another. And it's a really important concept to understand.

Darren Wurz [00:02:02]:

Right.

Darren Wurz [00:02:03]:

You know, we can apply this in so many ways, so many parts of our life time, you know, opportunity costs in terms of time. You know, our time is so strained as business owners and as a law firm owner, I bet yours is too.

Darren Wurz [00:02:16]:

Right.

Darren Wurz [00:02:17]:

But when you're focused on organizing your inbox, the question isn't, you know, is that a waste of time or not? The question is, what could you be doing with that time spent elsewhere?

Darren Wurz [00:02:29]:

Right.

Darren Wurz [00:02:29]:

That's opportunity cost. You're thinking about it.

Darren Wurz [00:02:31]:

The Right way.

Darren Wurz [00:02:32]:

So with student loans, it's not just, should I pay this off? It's what am I not doing with this money? Instead, if you're throwing every extra dollar at your loans, what are you leaving on the table? Here are some things you could be doing instead. Investing in your retirement. Building a marketing machine for your law firm. Hiring so you can free up time. Buying real estate so you can generate passive income. Taking a vacation so you don't burn out. All great things. You know, here's the thing.

Darren Wurz [00:03:04]:

Paying off your loans aggressively feels productive. It feels great, right? We're making progress. But sometimes it's a low return use of your capital, especially when loan interest rates are lower and your business has a higher ROI return on investment potential. So ask yourself, what could I do with this money that might grow my wealth faster, build my firm faster, or reduce my stress faster? Because let's face it, that can be equally important, that can pay huge dividends. Okay? Opportunity cost isn't always about percentages. Sometimes it's about other things like freedom, peace of mind, growth, you know, personal growth and development. So let's talk about a decision framework. You know, decision framework to help you choose the best strategy for you.

Darren Wurz [00:03:58]:

First, let's break down the math because, yes, there's a math side of things, okay? The logical part, the logical way to make the best decision with excess cash is to compare interest rates. We're looking for the best roi, folks. Your interest rates. Think of your student loans as having an roi. The ROI on your and your student loans, by paying them down, you're not incurring the cost of interest. So the ROI on your student loans is the interest. But what kinds of ROI could you get elsewhere? Run, break even, you know, and the best way to do this is to run a break even analysis. If I take this money and instead of, you know, I have an extra thousand dollars a month or I have an extra $2,000 a month, if I took this money and I put it in this or I invested in that, at what point would I have enough money to pay these loans off completely? And would that be faster than just putting the money in the loans directly? And would it save me more money? Would it make me more money? So a break even analysis.

Darren Wurz [00:05:05]:

How do I do that? Well, I'm going to walk you through it, okay? Also ask yourself 10 to 20 years from now, which option leaves me with the most money? That's what we want, right? We want to figure that out. On the logical side, if you're someone who wants the Cold hard numbers, run the projections. And a good planner, by the way, like us here at the Lawyer Millionaire Founders Network, we can help you do just that. All right, folks, so I'm going to give you an example. And I'm taking this example directly from my book, by the way, the Lawyer Millionaire, published by the American Bar Association. You can get your copy on Amazon or at the ABA Bookstore. So I'm going to read, I'm just going to read this. I'm just going to read this right from my book, this example.

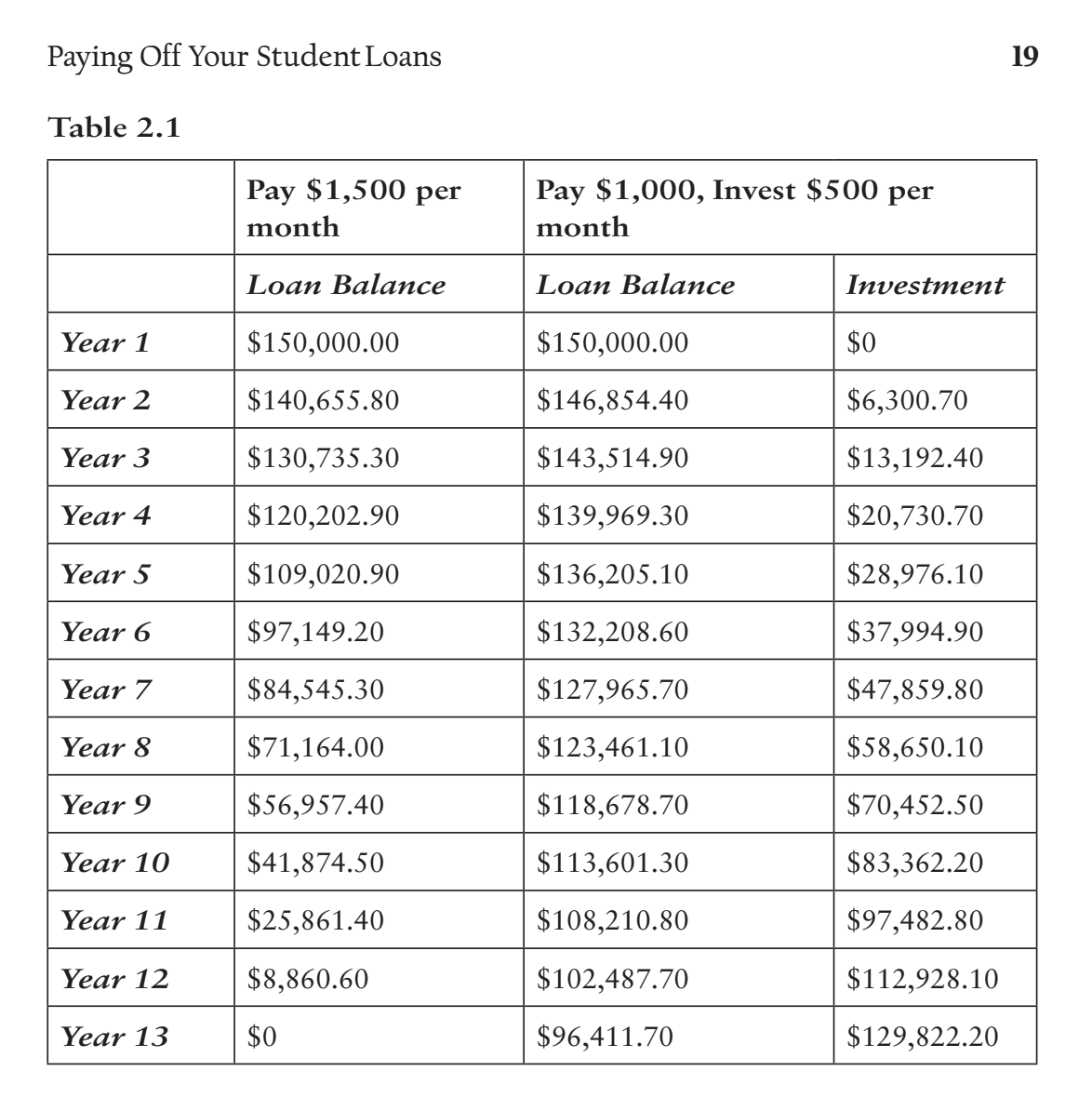

Darren Wurz [00:05:46]:

Okay, so here it is. Suppose you have $150,000 in student loans with an interest rate of 6% will assume the interest is capitalized or added to the principal. In other words, your minimum payment according to your payment plan, let's say, is $1,000 a month. But you could pay $1,500 a month, so you have an extra $500. If you put all of the $1500 toward your student loans, you'll have paid them off in 12 years. And by the way, I have a whole table here in the book. So what I'll do actually is I'm going to put this in a little document and you can download it in the show notes, okay? So you can see the actual chart. I'll put the chart in there for you.

Darren Wurz [00:06:26]:

So 12 years, you got an extra $500, you can pay off your student loans in 12 years. If on the other hand, you were to take that and you were to just pay the minimum thousand dollars a month and invest the extra $500 a month in the stock market S&P 500, good old fashioned passive low cost index fund like SPY or something. Let's assume a 9% average annual interest rate at the end of 12 years, you could accumulate $29,822. So roughly $130,000 in your investments by the end of year 12, which would be more than enough to pay off the balance left over at that point and still have $33,000 left over. So in other words, if you just pay the minimum and Instead over that 12 years, you were to invest the extra $500, you would have a whole lot more money. You would have your loan balance at year 13 would be 96,000. You'd pay that off with 130. So you'd have, you know, $34,000 from that, plus you would have.

Darren Wurz [00:07:39]:

No, okay, I'm sorry, you would have an extra $33,000. Okay? So net case altogether at the end of 12 years, if you invested the excess cash, you would have an extra $33,410.

Darren Wurz [00:07:55]:

Wow.

Darren Wurz [00:07:55]:

How about that? So who doesn't want an extra $33,000? I sure do. Now, that doesn't get you as far as it used to. Right. But that's a great example. So now it all comes down to the delta, the difference between your student loan balance, I'm sorry, your student loan interest rates and your rate of return that you can get. Now, there is a caveat here, because in the markets, as we know, we don't get a, you know, even rate of return every single year. Markets have great years sometimes. Some years we have much more than that.

Darren Wurz [00:08:29]:

Some years we have 20% return or more in the markets. We've had a lot of those years over the past few years. Some years are negative now, those tend to be far and fewer between. But it does happen. So that is something to be aware of. And so a big component of this is assessing your risk tolerance. Are you tolerant of the fact that your investments may fluctuate and that 9% rate of return isn't guaranteed? It might actually be less. It might actually be more.

Darren Wurz [00:08:57]:

Okay, well, let's think about this from a law firm owner's perspective instead. What if instead of investing in the market, you invested in your business? The ROI there could be a whole lot more.

Darren Wurz [00:09:12]:

Right.

Darren Wurz [00:09:13]:

Let's say you took the extra money that you have and you used it to outsource some of your intake to someone in the Philippines.

Darren Wurz [00:09:22]:

Right.

Darren Wurz [00:09:23]:

This could maybe free up more time for you so you could take on more cases and have more profit. And in that case, you could have 100%, 200%, 300% return on your investment as 5% at your student loans. But there's risk there, of course, as well. You have to think about the risk. And are you actually going to be able to generate the ROI that you expect in your business? So it all comes down to the interest rate. Yes, but we need to understand also the risk involved. The student loans are going to get that interest rate every single year, guaranteed.

Darren Wurz [00:10:01]:

Right.

Darren Wurz [00:10:01]:

They're going to charge that interest rate no matter what. Now, you're not guaranteed to get an ROI on the investments you make in your business. So that's why you want to be smart about the investments that you're making in your business.

Darren Wurz [00:10:15]:

Right.

Darren Wurz [00:10:16]:

And make sure that those are going to directly increase profit if you're going to make that decision instead. So, yes, the math matters. You know, paying off debt is safe and simple. It feels that way. It feels safe. It feels Simple. And so many people opt to just do that and throw their extra dollars towards paying off their student loans. But investing, whether in your in the market or in your business, is where the real wealth is built.

Darren Wurz [00:10:41]:

The trick is aligning your math with your mindset and your goals.

Darren Wurz [00:10:48]:

Right?

Darren Wurz [00:10:49]:

How much risk are you comfortable taking? Are you comfortable taking some risk in the markets or in your business? Then maybe that should be where you go. But we also have to think about how you feel about it. So there is the psychology side of things. Do you get anxious every time you see your student loan balance? Do you feel free knowing your debt is gone? Or would you feel free knowing your debt was gone even if it wasn't the smartest math move? We read the Psychology of Money in the Lawyer Millionaire book club and one of the things he talks about is it's not always about getting the highest rate of return. Sometimes it's about doing the thing that's going to make you sleep better at night. Or on the other hand, do you get excited about the idea of your investments compounding while your debt slowly disappears. So you really need to understand your psychology and your risk tolerance. A great financial decision is one that aligns both.

Darren Wurz [00:11:50]:

It aligns your mind and your money, your logic and your emotions. But I want to talk about one thing here that sometimes gets in the way on the subject of psychology. Let's dig into. Let's dig a little bit deeper into why many times we don't follow the math. There's a concept called behavioral concept called hyperbolic discounting. It's a fancy term that means we tend to irrationally prefer smaller immediate rewards over bigger delayed ones. I'll say it again. We prefer smaller immediate rewards versus bigger ones.

Darren Wurz [00:12:31]:

That may happen. We may have to wait for. It's related to this idea of delayed instant gratification. We want it now. It's my money and I want it now. That's why people often choose the snowball method, paying off the smaller loans first, even though the math doesn't make as much sense logically because they want that fast win, even if it's less efficient. It's why people choose a loan payoff over investing because it gives them a sense of control and closure. When I put money on my student loans, wow.

Darren Wurz [00:13:07]:

I can see it happen right now. I can see the balance going down right now. And it just feels good. But hyperbolic discounting is also why people delay making a decision entirely because the future feels fuzzy and the present feels urgent. You know what I hear a lot of people Often say, they say, I just hate seeing the balance. I just want it to go away. And this happens in retirement, too. I see this a lot.

Darren Wurz [00:13:32]:

Clients who have a mortgage at a 2.5% interest rate and they're like, I just want to pay it off. I don't want to be paying a mortgage anymore. I just don't want to have this payment anymore. Even though not having the payment isn't what's going to make them more wealth in the long run, not having the payment is just going to make them feel better in the present.

Darren Wurz [00:13:55]:

Right?

Darren Wurz [00:13:56]:

That's hyperbolic discounting. How do we fix that? How do we trick ourselves? Well, one, make long term benefits feel more immediate and emotionally rewarding. How do you do that?

Darren Wurz [00:14:09]:

While.

Darren Wurz [00:14:10]:

Well, here are some ideas for you. Pre commitment. Okay, so pre commitment means setting things up on autopilot, basically, so I don't have to think about it. Don't look at your loans anymore.

Darren Wurz [00:14:20]:

Right?

Darren Wurz [00:14:21]:

Set up that investment strategy on autopilot. Automate as much as possible. Reward substitution. Basically, celebrate small milestones where you may feel the reward of paying off your student loans and seeing that balance go down a little bit. Instead, reward yourself for what you're doing. Instead, reward yourself for putting money in your Roth ira. Yeah, celebrate that. Another tactic is visualization of the future self.

Darren Wurz [00:14:49]:

Think about your future self 10, 20, 30 years from now. Say it to yourself at age 47, at age 57, at age 67, and envision yourself at that age. Well, what will you have wanted to do? Which decision will have caused you the least regret? Shrink the delay. Another tactic. Instead of in 20 years, if I follow this method of investing more, instead of paying off the loans faster, in 20 years, I'll have X shrink the delay and say to yourself, if I invest this month, I am X closer to I'm $100 closer to financial freedom. You've got to trick yourself. Use identity framing. So give yourself identity statements.

Darren Wurz [00:15:39]:

I'm the kind of person who makes strategic decisions with their money. I invest every month because I'm the CFO of my life, right? Identify yourself as the kind of person that does this. And lastly, reframe the benefit of not paying off your loans early. What could that do for you? Instead, reframe the benefit. There's a benefit to not paying off your loans early. You could hire an associate this year. Take Fridays off. Grow your firm faster.

Darren Wurz [00:16:11]:

Grow your investments faster. Get to financial freedom faster.

Darren Wurz [00:16:15]:

Right?

Darren Wurz [00:16:15]:

Reframe the benefits. Once the reward becomes real and immediate, you will stick with the smart plan. Okay, so here's the final truth. Not making a decision is a decision. Sometimes. A lot of people probably have been just burying their head in the sand on their student loans for these past few years, not having to think about them. Every day you wait, your student loan balance grows. So the worst thing you could do is just ignore it altogether.

Darren Wurz [00:16:46]:

Because your loans just grow. Time passes, opportunities are missed. Whether it's ignoring them completely, failing to lock in a good refinance rate when they happen. Watch for rates. Rates are high. Ish right now. Historically they're pretty low. But next time rates come down might be a great moment for you to refinance or missing the compounding of early investments.

Darren Wurz [00:17:10]:

Not taking action has a cost. So ask yourself the right questions. Not just what should I do? But what matters most to me? What's the smartest use of my next dollar? And what's the future that I want to build? My challenge to you this week is to run your numbers, but also check in with your mindset. Ask yourself, am I choosing the path that builds wealth or just the one that feels comfortable now?

Darren Wurz [00:17:37]:

Right.

Darren Wurz [00:17:37]:

The smartest decisions blend the two. Logic and emotion. Make sure your strategy reflects both, but don't give in totally to your emotion.

Darren Wurz [00:17:47]:

Right? But.

Darren Wurz [00:17:47]:

But respect it. At the Lawyer Millionaire, we believe that every financial decision, whether it's paying off your loans, investing or growing your firm, is a step toward long term wealth and financial freedom. Our job is to help you build a business that funds your lifestyle now and creates lasting financial success for your future. You don't have to figure it out all alone. That's the beautiful thing. We work with law firm owners just like you to help you map out strategies that align your goals, your cash flow, and your values. If you want to learn more about how we can help you pay down your student loans, build wealth, and get to financial Freedom faster, visit lawyermillionaire.com, download the first chapter of my book for free. It's the Lawyer Millionaire, by the way.

Darren Wurz [00:18:40]:

And if you want to grow your mindset alongside other ambitious law firm owners just like you, you should definitely join our book club community for free. The link is in the show notes. Who is the Lawyer Millionaire? My friend, it's you. Own it and live it. I'm your host, Darren Wirtz. Thank you so much for joining me. I'll see you next time. My challenge to you this week is to run your numbers, but also check in with your mindset.

Darren Wurz [00:19:10]:

Ask yourself, am I choosing the path that builds wealth or just the one that feels comfortable right now. The smartest financial decisions blend logic and emotion. Make sure your strategy reflects both. At the Lawyer Millionaire, we believe every financial decision, whether it's paying off your loans, investing or growing your firm, is a step toward long term wealth and freedom. And our job is to help you build a business that funds your lifestyle now and creates lasting financial success for your future. You don't have to figure it out all by yourself. We work with law firm owners just like you to help you map out strategies that align with your goals, your cash flow and your values. If you enjoyed today's episode, help us out by entering our Lawyer Millionaire Listener Challenge.

Darren Wurz [00:19:59]:

Listen, leave a review, share an episode and submit your entry at lawyermillionaire.com/challenge for a chance to win. And if you want to talk one on one, you can always book an intro call with me using the link in the show notes. Who is the Lawyer Millionaire? It's you, my friend. Own it and live it. I'm your host, Darren Wurz. Thank you so much for joining me. See you next time.